stock market INSIDE INFORMATION

Countdown to 2025: Wrap Up Your Finances with Style

The end of the year is approaching faster than a Black Friday deal, and that means it's time to whip your finances into shape. From tax moves to portfolio adjustments, now’s the perfect moment to prepare for a prosperous new year. Don’t leave these tasks for December 31st—future you will thank you. Here’s your 9-step guide to closing out 2024 like a financial pro!

Bullvora Research Team

11/18/20243 min read

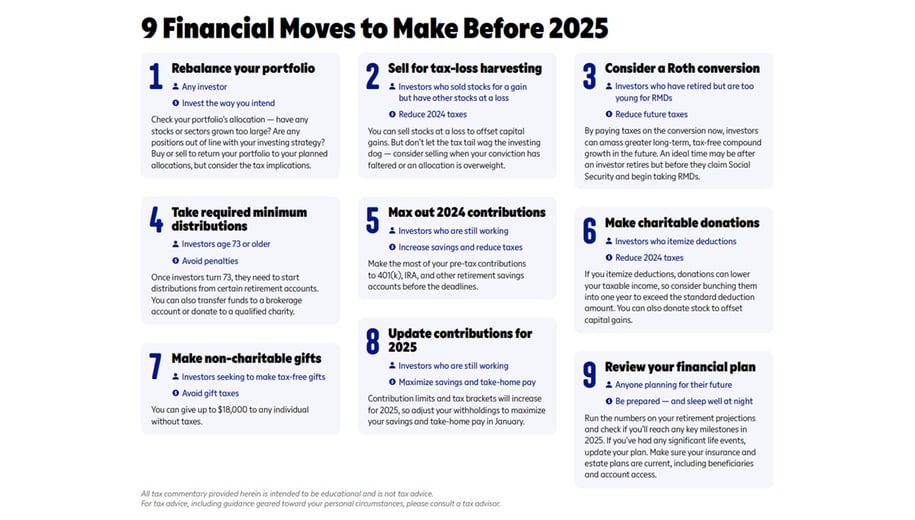

MOVE 1: Rebalance Your Portfolio

What’s the Deal?

Markets don’t stand still, and neither should your portfolio. Revisit your asset allocation to ensure it’s still aligned with your goals. Too much exposure in one area? Time to trim it down.

Why It Matters:

A winner running wild can distort your portfolio. Stocks ballooning to over 15% of your holdings? Reign them in to avoid unnecessary risk. The same goes for sectors—no single industry should dominate more than 40% of your investments.

Pro Tip:

Keep some cash on hand for expenses within the next 3–5 years. Stocks are great, but they don’t pay for emergencies on time.

MOVE 2: Tax-Loss Harvesting

What’s the Deal?

Turn losses into gains—sort of. Selling underperforming stocks can offset taxable gains and potentially lower your tax bill.

Why It Matters:

Short-term losses offset short-term gains; long-term losses tackle long-term gains. It’s tax efficiency 101.

Watch Out:

Beware the wash sale rule—if you buy back a similar stock within 30 days, the IRS will void your tax benefit. And if you’re in the 0% tax bracket for long-term capital gains? Skip this move entirely.

MOVE 3: Roth IRA Conversion

What’s the Deal?

Convert traditional IRA funds into a Roth IRA for long-term, tax-free growth. Pay taxes now, enjoy tax-free withdrawals later.

Why It Matters:

If you expect higher taxes in retirement, this could be a savvy move. Just make sure you have the cash to cover the tax bill without dipping into your retirement savings.

When’s the Sweet Spot?

Between retirement and claiming Social Security—your income is lower, and tax rates might be kinder.

MOVE 4: Required Minimum Distributions (RMDs)

What’s the Deal?

Once you hit 73, Uncle Sam insists you withdraw a minimum amount from most retirement accounts.

Why It Matters:

Miss your RMD? Expect a penalty of up to 50% of what you should’ve taken out. No thanks!

Pro Move:

Don’t need the cash? Use a qualified charitable distribution (QCD) to donate directly to a charity. It’s a win-win—good for your taxes and your karma.

MOVE 5: Max Out Retirement Contributions

What’s the Deal?

Whether pre-tax (lower this year’s tax bill) or Roth (tax-free withdrawals later), don’t miss the chance to maximize 2024 contributions.

Why It Matters:

Every dollar counts toward compounding growth. Invest in your future self while slashing your current tax burden.

MOVE 6: Make Charitable Donations

What’s the Deal?

Support causes you care about while scoring a potential tax deduction. Just make sure you itemize!

Why It Matters:

Standard deductions are high these days, but if you’re close to crossing into itemizing territory, donations could tip the scales.

MOVE 7: Use Your FSA Funds

What’s the Deal?

Got a Flexible Spending Account (FSA)? Use it or lose it—most plans don’t let you carry over funds past December 31st.

Why It Matters:

Unused funds disappear into the financial ether. Schedule that doctor’s visit, stock up on glasses, or snag some health-related products before it’s too late.

Pro Tip:

Some plans allow a rollover of up to $610—double-check with HR.

MOVE 8: Double-Check Withholding and Estimated Taxes

What’s the Deal?

Owe taxes this year? Avoid penalties by ensuring your withholdings or estimated payments are on track.

Why It Matters:

Underpayment penalties are like throwing money into a void. Use the IRS withholding calculator to make adjustments if needed.

Pro Move:

Overpaid? Use your refund to boost retirement savings in 2025.

MOVE 9: Review Your Estate Plan

What’s the Deal?

Year-end is the perfect time to make sure your estate plan reflects your wishes.

Why It Matters:

Life changes (marriage, kids, big promotions) can shift your financial landscape. Keep your will, beneficiaries, and power of attorney documents updated.

Bonus Tip:

Don’t forget digital assets—assign someone trustworthy to manage your online presence.

Cheers to 2025!

With these 9 financial moves checked off your list, you’ll be ready to ring in the new year like a seasoned investor. Here’s to a new year filled with growth, success, and maybe even a few extra zeros in your portfolio!

Stay Connected for Hot Daily Updates!

Email: bullvora@bullvora.com

Phone: 1 (800) 589-3380

© 2024. All rights reserved.